Getting there, but slowly

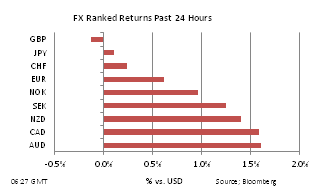

After an all-nighter in Brussels, European leaders have finally announced a package of measures which they hope will placate the concerns of investors and traders regarding the sovereign debt and banking crisis. The package has three major components ? the firepower of the EFSF has allegedly been raised to EUR 1.4trln, Greek debt-holders have apparently accepted a 50% haircut, and European banks are to be recapitalised. Also announced was a more significant role for the IMF (although exactly what that role will be is not yet clear), and the continued involvement of the ECB with respect to buying the bonds of troubled European sovereigns in the secondary market. These measures have literally just been announced in the last couple of hours and as a result, fuller analysis will follow over the course of the day. Suffice to say at this stage, European policy-makers appear to have done enough for now to encourage the belief that they are finally facing up to the true extent of their difficulties. In response, the EUR is up above 1.40, the dollar is weaker, metal prices are higher and Asian equities are up by more than 2%.

Commentary

Berlusconi’s last days in power? Italian Prime Minister Berlusconi’s obituary has been written many times before, only for the Teflon-coated leader to defy the odds. This time, however, his days do truly look numbered. His fragile coalition was placed under the most intense pressure from European leaders to undertake substantive structural reforms in order to reshape Italy’s sclerotic economy. Overnight, he committed to raise EUR 5bn per year from asset sales, lift the pensionable age and undertake labour market reform. Germany in particular, joined by France, demanded that Berlusconi deliver on these reforms before they agreed to raise the firepower of the EFSF. A major sticking point for the fragile coalition was pension reform. There was a wonderful remark from the head of the Northern League Umberto Bossi earlier this week which highlights why this strikes such a raw nerve in Italian politics – Bossi claimed that “if we touch pensions the people will kill us”. If Berlusconi’s coalition fractures over this issue, there is a distinct likelihood of snap elections, and with the stain on Berlusconi’s reputation after recent scandals he may not survive. At such an incredibly sensitive time for Italy, fresh political uncertainty would only heighten the country’s financial difficulties.

Chinese policy-makers are turning. Against the backdrop of slower growth in Europe and the rest of the world, and with the local economy clearly responding to the significant tightening in monetary policy, Chinese policy-makers are starting to adopt a slightly more accommodating tune. Yesterday, Chinese Premier Wen Jiabao suggested that economic policy would be ”fine-tuned”, while the industry ministry is studying fresh initiatives to aid small businesses. The director-general of the industry ministry also observed that the pace of output growth was likely to slow both this quarter and next year. With inflation still above 6%, it is too soon to expect any relief on interest rates, although what is probably being considered is some reduction in bank reserve requirements which have been lifted appreciably over the past year. Good news then for risk-takers – the major advanced economies continue to implement ultra-loose monetary policy and now it appears that the world’s second largest economy is considering the merits of making financial conditions a little easier.

UK manufacturing pessimism deepens. After Tuesday’s positive news that Britain was rebalancing, we were reminded yesterday that the state of the economy remains fairly dire. According to the latest survey from the CBI, its measure of business optimism dropped sharply in the three months ended October to -30, from -16 previously, the lowest reading since April 2009. Manufacturers have been hit by a significant decline in orders, which will impact on activity levels in coming months. Clearly, the uncertainty in Europe is weighing heavily on overall confidence. Indeed, the CBI expects manufacturing production to decline by 0.6% in the current quarter, after a 0.2% increase in Q3. The Bank of England will also be interested in the reduction in selling expectations recorded in the survey. Other than reduced price pressures, there was nothing else in this survey to provide any comfort.

Aussie rate-cut a near certainty now. A rate cut of at least 25bp down under now looks a near certainty next week when the RBA meets following benign inflation figures for the third quarter released yesterday. Although the headline CPI outcome for Q3 was as expected (0.6%), it was the low readings for core inflation that were especially encouraging. The RBA’s trimmed mean gauge of inflation was up just 0.3% in the third quarter, a rise of 2.3% from a year earlier. Together with the growing evidence of recent months showing that the economy has slowed quite markedly, the case for at least one rate cut before year-end and possibly two is now compelling. Looking further ahead into 2012, the front end of the yield curve expects that the RBA will ease monetary policy still further, by another 50bp before the middle of the year. In response to the latest inflation figures, the Aussie understandably dipped back below 1.04, although to be frank the damage was relatively minimal after what has been a fabulous run. Since early this month, the Aussie has soared by ten big figures from the low; unsurprisingly, it is the best-performing major currency for October. Against the backdrop of a weakening economy, and with the central bank possibly on the cusp of a significant monetary policy-easing cycle, it has been an impressive performance. One of the explanations for the incredible recovery is that the huge US money market funds have been diverting exposure to Europe into ‘safer’ locations like Australia. According to a Fitch survey of these US money market managers, Australian debt exposure accounted for a staggering 9.4% of assets under management at the end of last month. Australian banks are regarded as among the strongest in the world right now and the yield on offer for short term debt is well over 5%. While Europe burns, Australia is making hay...

Commentary

Berlusconi’s last days in power? Italian Prime Minister Berlusconi’s obituary has been written many times before, only for the Teflon-coated leader to defy the odds. This time, however, his days do truly look numbered. His fragile coalition was placed under the most intense pressure from European leaders to undertake substantive structural reforms in order to reshape Italy’s sclerotic economy. Overnight, he committed to raise EUR 5bn per year from asset sales, lift the pensionable age and undertake labour market reform. Germany in particular, joined by France, demanded that Berlusconi deliver on these reforms before they agreed to raise the firepower of the EFSF. A major sticking point for the fragile coalition was pension reform. There was a wonderful remark from the head of the Northern League Umberto Bossi earlier this week which highlights why this strikes such a raw nerve in Italian politics – Bossi claimed that “if we touch pensions the people will kill us”. If Berlusconi’s coalition fractures over this issue, there is a distinct likelihood of snap elections, and with the stain on Berlusconi’s reputation after recent scandals he may not survive. At such an incredibly sensitive time for Italy, fresh political uncertainty would only heighten the country’s financial difficulties.

Chinese policy-makers are turning. Against the backdrop of slower growth in Europe and the rest of the world, and with the local economy clearly responding to the significant tightening in monetary policy, Chinese policy-makers are starting to adopt a slightly more accommodating tune. Yesterday, Chinese Premier Wen Jiabao suggested that economic policy would be ”fine-tuned”, while the industry ministry is studying fresh initiatives to aid small businesses. The director-general of the industry ministry also observed that the pace of output growth was likely to slow both this quarter and next year. With inflation still above 6%, it is too soon to expect any relief on interest rates, although what is probably being considered is some reduction in bank reserve requirements which have been lifted appreciably over the past year. Good news then for risk-takers – the major advanced economies continue to implement ultra-loose monetary policy and now it appears that the world’s second largest economy is considering the merits of making financial conditions a little easier.

UK manufacturing pessimism deepens. After Tuesday’s positive news that Britain was rebalancing, we were reminded yesterday that the state of the economy remains fairly dire. According to the latest survey from the CBI, its measure of business optimism dropped sharply in the three months ended October to -30, from -16 previously, the lowest reading since April 2009. Manufacturers have been hit by a significant decline in orders, which will impact on activity levels in coming months. Clearly, the uncertainty in Europe is weighing heavily on overall confidence. Indeed, the CBI expects manufacturing production to decline by 0.6% in the current quarter, after a 0.2% increase in Q3. The Bank of England will also be interested in the reduction in selling expectations recorded in the survey. Other than reduced price pressures, there was nothing else in this survey to provide any comfort.

Aussie rate-cut a near certainty now. A rate cut of at least 25bp down under now looks a near certainty next week when the RBA meets following benign inflation figures for the third quarter released yesterday. Although the headline CPI outcome for Q3 was as expected (0.6%), it was the low readings for core inflation that were especially encouraging. The RBA’s trimmed mean gauge of inflation was up just 0.3% in the third quarter, a rise of 2.3% from a year earlier. Together with the growing evidence of recent months showing that the economy has slowed quite markedly, the case for at least one rate cut before year-end and possibly two is now compelling. Looking further ahead into 2012, the front end of the yield curve expects that the RBA will ease monetary policy still further, by another 50bp before the middle of the year. In response to the latest inflation figures, the Aussie understandably dipped back below 1.04, although to be frank the damage was relatively minimal after what has been a fabulous run. Since early this month, the Aussie has soared by ten big figures from the low; unsurprisingly, it is the best-performing major currency for October. Against the backdrop of a weakening economy, and with the central bank possibly on the cusp of a significant monetary policy-easing cycle, it has been an impressive performance. One of the explanations for the incredible recovery is that the huge US money market funds have been diverting exposure to Europe into ‘safer’ locations like Australia. According to a Fitch survey of these US money market managers, Australian debt exposure accounted for a staggering 9.4% of assets under management at the end of last month. Australian banks are regarded as among the strongest in the world right now and the yield on offer for short term debt is well over 5%. While Europe burns, Australia is making hay...

No comments:

Post a Comment